8 / 61

8 / 61

Insight Perspectives

Insight Perspectives

7

At this stage, the European economy does not need

more monetary stimulus. The European economy is

assessed by this newsletter to be mid-cycle - see

Insightperspectives’ “real time”

economic cycle .The

economy benefits from an ultra-loose monetary policy

and, ironically, the ECB’s failure to create inflation in

spite of a weak euro. At present, the best leading

indicators in Europe are still harbingers of strong

demand in the manufacturing and service sectors, at

least in the very near future.

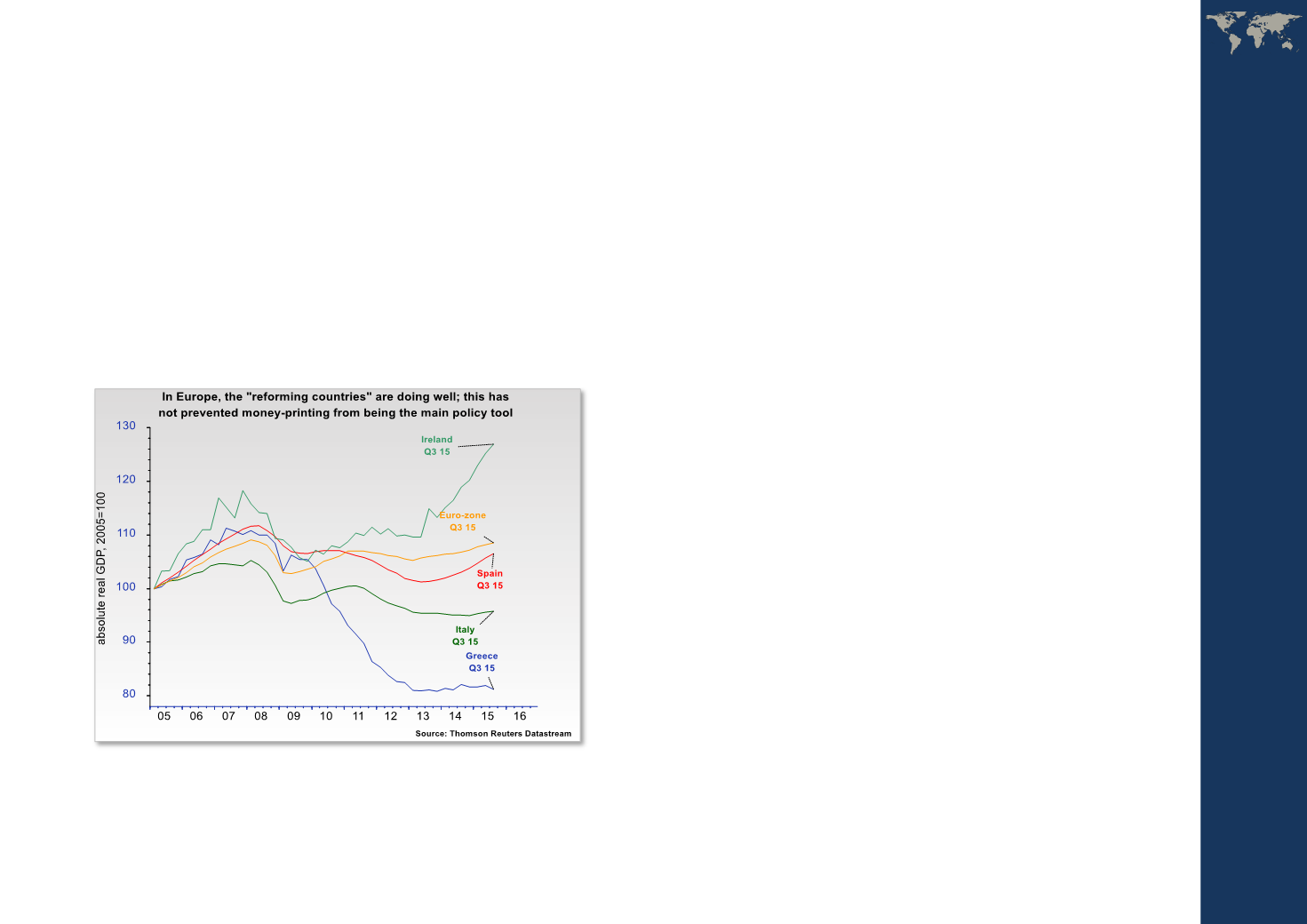

The problem is that the improvement is predominantly

based on front-loading of "future growth" and a

beggar-thy-neighbour-policy caused by the ECB’s very

aggressive monetary policy. Indeed, only few countries

in the Euro-zone (Spain, Portugal and Ireland) have

seen an economic recovery based on real improvement

in macroeconomic fundamentals. This is also why

Europe’s corporate sector may prove hesitant when it

comes to boosting investment.

The latter is the case not least if the refugee crisis

creates significant headwind, which may dent the

current strong cyclical tailwind. The political impact of

the refugee crisis has only just started and will become

even more visible if Brussels (or more precisely Berlin)

decides to force member countries to take more

refugees as part of the latest deal with Ankara - read

the Bloomberg article,

Hungary's Orban Says Germany Struck `Secret' Turkey Refugee Deal .Germany – Solid short-term growth; but “wir

schaffen dass nicht” gains momentum

Germany is at the center of the European refugee crisis.

So far, however, this has not been negative for growth,

at least not until recently. Manufacturing sentiment

remains relatively upbeat. This is the case even though

the

leading IFO manufacturing headline index fellmarginally to 108.7 in December from 109.0

in November. The IFO service index, however, rose to