4 / 61

4 / 61

Insight Perspectives

Insight Perspectives

3

exposed to cyclical tailwind. Ironically, this is not least

due to the fact that ECB president Draghi failed to

create inflation, which has refueled households’ real

purchasing power. In the first half of 2016, low inflation

will probably prevail in the global economy due to weak

demand; but this could end abruptly when demand

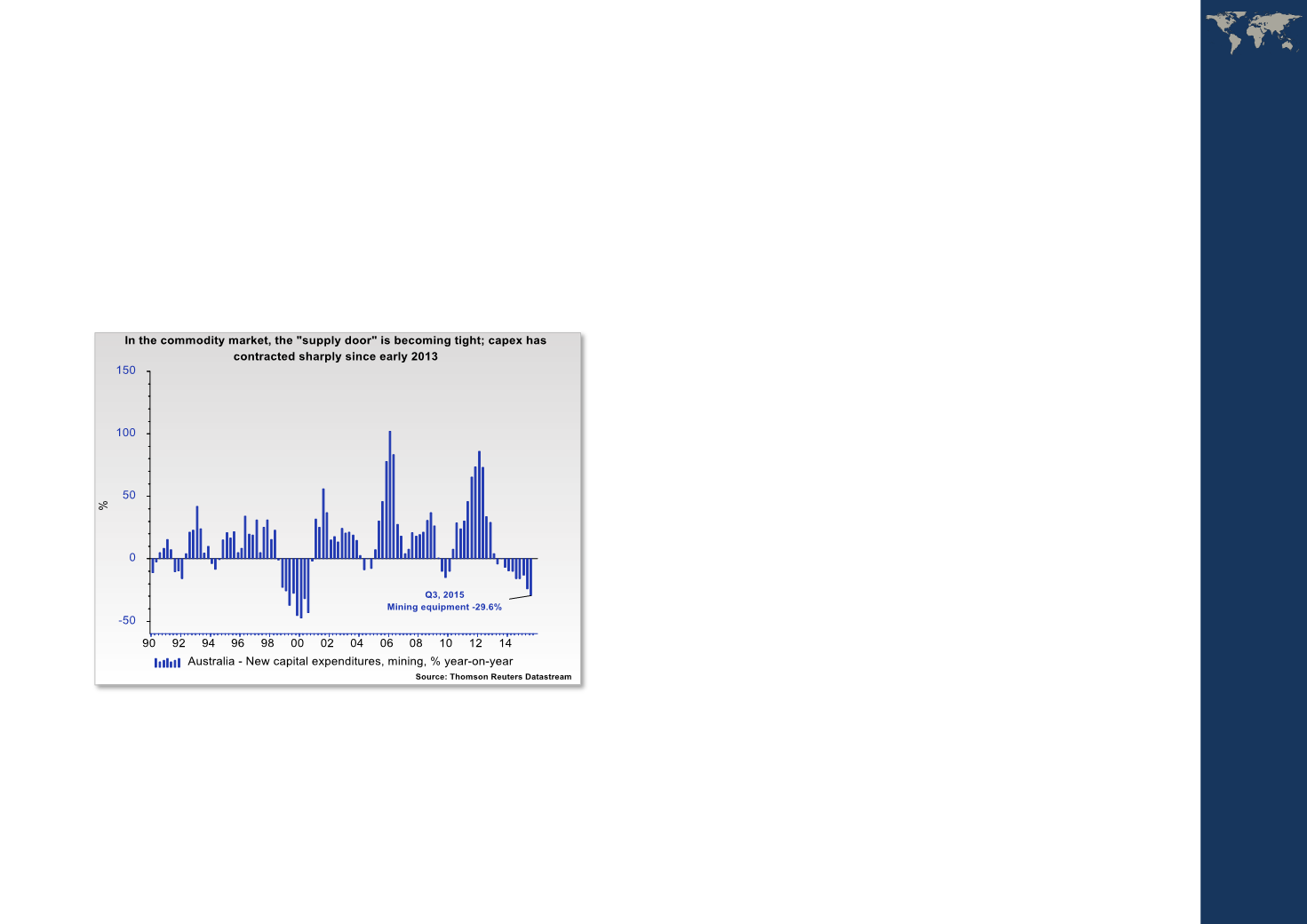

finally recovers, as plunging capital exenditure in the

mining sector has made the “supply door” rather tight.

In Europe, the political situation could create significant

headwind in 2016 from several directions. Granted, the

biggest short-term “threat” failed to show up in

December as

Front National, a far-right party, did not gain a landslide victoryin regional elections in France,

as the political establishment united its forces against

the party in the second round.

On the other hand, the

outcome of Spain’s national elections in December made the country yet another fragile factor in the European Union. The balance of powerwas

radically

changed;

the

political

establishment, the Popular Party and the Socialist

Party, are forced to either form a grand coalition or

work together with the two newcomers,

Podemos(far-

left) or

Ciudadanos(ultra market-liberal). The only

positive factor, at least from a financial market point of

view, is that the Socialists and

Podemosare not able to

establish a majority.

Whereas the outcome of Spain’s national elections is

part of the aftermath of the financial crisis in 2008-

2009, the ongoing refugee crisis could prove far more

dangerous to Europe’s financial market in 2016. This is

because Chancellor Merkel’s autocratic decision-

making in connection with the refugee crisis has

endangered cohesion in the European Union. This has

made many small EU member countries reconsider

their position when it comes to deeper European

integration, which was probably also part of the

explanation behind the Danish “No” on December 3 to